Buying a property is likely the biggest purchase you will ever make. It is an exciting process, but it can also be confusing. You hear terms thrown around like ‘agreement to sale’ and ‘sale deed’. They sound similar, right?

Many people assume they are the same thing. That is a costly mistake.

Confusing these two documents can lead to serious legal and financial trouble. You might think you own a house when you actually don’t. You could lose your hard-earned money.

Let’s clear up the confusion. In this guide, I will break down the difference between an agreement to sale and a sale deed. I will explain them in simple terms. By the end, you will know exactly what each document does and why they both matter.

What Is an Agreement to Sale?

Think of an Agreement to Sale as a promise. It is a written promise between a buyer and a seller. The seller promises to sell a specific property to the buyer in the future. The buyer promises to buy it.

It is not the final deal. It is a formal understanding of how the final deal will happen.

I recently helped a friend who was buying an apartment in a new building. The building was still under construction. The first document he signed was the Agreement to Sale. It laid out all the ground rules.

Key Features of an Agreement to Sale

This document is like a roadmap for the transaction. It includes several important details:

- Property Details: It clearly describes the property. This includes the exact location, size, and apartment number.

- Sale Price: The total agreed-upon price is mentioned here.

- Payment Schedule: This is a crucial part. It details how much you pay and when. It might say, “Pay 10% on signing, 30% when the foundation is laid,” and so on.

- Possession Timeline: It promises a date or a timeframe for when you will get the keys to the property.

- Terms and Conditions: It covers what happens if something goes wrong. For example, what if the builder delays the project? What if the buyer can’t get a loan? The agreement outlines the penalties and cancellation terms.

Legal Status of an Agreement to Sale

Here is the most important thing to remember:

An Agreement to Sale does not transfer ownership.

Legally, it is known as a ‘executory contract’. That means something still needs to happen. In this case, the ‘something’ is the final sale. The ownership of the property stays with the seller. You only get the right to demand that they sell it to you later, as long as you stick to the terms.

Think of it like booking a flight. You pay a deposit and get a ticket confirmation. That confirmation is like the agreement to sale. It guarantees you a seat on a specific flight on a future date. But, you don’t own the seat until you actually get on the plane. If you miss the flight, you might lose your money or have to pay a fee.

Sometimes, this document is part of a larger deal. For instance, if you are getting a house built, you might sign a house construction agreement between owner and contractor. This is similar, but it focuses on the building work. An Agreement to Sale is specifically about transferring the property itself. You might also see a building construction agreement or a labour contract agreement for construction of a house, which are different contracts focused on the actual building work, not the sale.

What Is a Sale Deed?

If the Agreement to Sale is the promise, the Sale Deed is the actual delivery.

A Sale Deed is the final legal document. It is the document that actually transfers the ownership of the property from the seller to you, the buyer. Once this is signed and registered, you become the official, legal owner.

Key Features of a Sale Deed

The Sale Deed is a comprehensive record of the transfer. It includes:

- Full Details of Parties: Complete information about the buyer and seller.

- Comprehensive Property Description: This is even more detailed than in the agreement. It often includes the property’s dimensions, boundaries, and title details.

- Sale Consideration: It clearly states the final amount paid for the property.

- Receipt of Payment: It confirms that the seller has received the full payment from the buyer.

- Indemnity Clause: This is a promise from the seller to protect the buyer if any legal issues with the property’s title come up later.

- Possession Clause: It officially states that the seller has handed over possession of the property to the buyer.

Legal Status of a Sale Deed

This is where ownership truly changes hands.

A Sale Deed is what lawyers call a ‘executed contract’. The action is complete. The deal is done. The property has been sold.

Ownership is transferred only after the Sale Deed is executed and registered.

It is your absolute proof of ownership. If anyone ever questions whether you own your home, this is the document you show them.

Agreement to Sale vs Sale Deed – Quick Comparison

Let’s look at the main differences side-by-side. This table makes it easy to see.

| Basis | Agreement to Sale | Sale Deed |

|---|---|---|

| Purpose | A future promise to transfer property. | The final transfer of ownership. |

| Timing | Signed before the sale, often months or years prior. | Signed at the completion of the sale. |

| Ownership | Ownership is not transferred. The seller still owns it. | Ownership is fully transferred to the buyer. |

| Registration | Registration is optional in many states, but it is highly recommended. | Registration is mandatory under the Registration Act, 1908. |

| Legal Strength | It is a binding contract. You can sue if the other party breaks the promise. | It is the ultimate legal proof of ownership. It is a document of title. |

Key Differences Explained in Detail

Let’s go deeper into what these differences mean for you.

1. Ownership Transfer

This is the core difference. With an Agreement to Sale, you have a right over the property. You have the right to buy it later. But the seller still holds the title. They are still the owner.

With a Sale Deed, the title passes to you. You become the owner. Your name is now on the legal record. The seller has no more claim to it.

2. Legal Validity

Both are legally valid, but in different ways.

The Agreement to Sale is a valid contract. It is enforceable under the Indian Contract Act. If the seller suddenly decides to sell the property to someone else for a higher price, you can go to court. You can ask the court to enforce the agreement.

The Sale Deed is not just a contract. It is the legal proof that the contract has been fulfilled. It is your primary document of title. It shows you are the lawful owner.

3. Registration Requirement

This is a practical difference that has big legal consequences.

An Agreement to Sale does not always need to be registered. It depends on the state and the specific terms. However, if the agreement also gives possession of the property to the buyer, then registration becomes mandatory. Even when it’s not mandatory, registering it is a smart move. It creates a public record and makes it harder for the seller to cheat you.

A Sale Deed must be registered. There is no option. You have to go to the Sub-Registrar’s office, pay the stamp duty, and get it officially recorded. Without registration, the Sale Deed has very little legal value.

4. Stamp Duty

Stamp duty is a tax you pay to the government on legal documents. The amount is different for these two documents.

Because the Agreement to Sale is not the final transfer, the stamp duty is much lower. It is often a fixed, nominal amount.

The Sale Deed is the main event. You pay the full stamp duty on the property’s value. This is a significant cost, often 5-7% of the property price, depending on your state. It is a major part of the total buying cost.

5. Risk Factor

Which one is riskier? They carry different kinds of risk.

The Agreement to Sale carries more ‘performance risk’. If the terms aren’t clear, you could face disputes later. What if the seller doesn’t build what they promised? What if they can’t get the necessary approvals? Your money is on the line, but you don’t own the property yet.

The Sale Deed is very secure. Once it’s registered, the deal is done. The risk is almost zero from a transfer perspective. However, there is still a risk if you didn’t do your homework. For example, if the seller didn’t have a clear title in the first place, even a registered Sale Deed could be challenged. That’s why you always verify the title before you pay.

When Is an Agreement to Sale Used?

You will typically encounter an Agreement to Sale in these situations:

- Under-construction Property: This is the most common use. You book an apartment in a new project. The building isn’t ready. The builder uses an Agreement to Sale to secure your commitment and outline the payment plan tied to construction milestones. It protects both of you until the building is finished.

- Delayed Possession Projects: Sometimes, a ready property can’t be handed over immediately because of paperwork or small pending issues. An agreement to sale can be used to book the property while those issues are sorted out.

- Installment-based Payment: If you are buying a property and paying in installments over time, the agreement to sale governs this period. It sets the rules for each payment until the final amount is paid and the sale deed is executed.

You might also see similar documents in other contexts. For example, a house construction contract agreement is used when you hire someone to build a house on your land. It is not a sale, but a contract for services. The house construction agreement format can vary, but its purpose is the same: to define the work and payment for construction, not the transfer of land ownership.

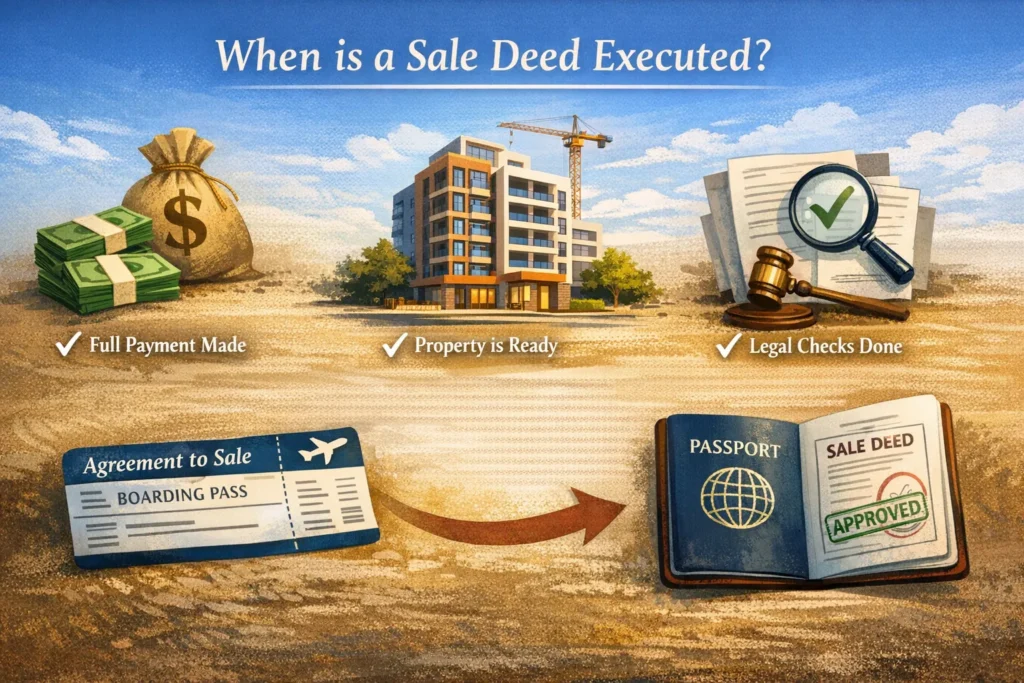

When Is a Sale Deed Executed?

The Sale Deed is the final step. It is executed only when everything is ready.

- Full Payment is Made: The buyer has paid the entire sale price. This includes the initial deposit and all subsequent installments. No money is left to pay.

- Property is Ready: For a new property, the construction is complete. The builder has obtained the completion certificate from the local authorities.

- All Legal Checks are Done: The seller has proven they have a clear and marketable title to the property. Any legal dues or encumbrances (like an unpaid loan using the property as collateral) have been cleared.

Think of the entire property purchase as a journey. The Agreement to Sale is the boarding pass you get at the start. The Sale Deed is the stamp in your passport when you finally arrive at your destination. It is the official record that you have entered and now belong there.

Important Clauses in an Agreement to Sale

When you read an Agreement to Sale, pay close attention to these clauses:

- Payment Terms: This is not just the total price. It is the schedule. Is it linked to construction stages? What are the due dates? Are there interest charges for late payment?

- Possession Date: Look for a specific date or a clear timeline. It should say something like, “on or before December 2025.” It should also state what happens if the seller delays. Will they pay you rent or a penalty?

- Penalties for Delay: This clause should work both ways. What penalty does the seller pay if they are late in giving possession? What penalty do you pay if you are late with a payment?

- Cancellation Terms: Understand how the agreement can be cancelled. Can the seller cancel if you miss a payment? Can you cancel if the project is too slow? Most importantly, what happens to the money you have already paid in case of cancellation? Will you get a full refund, or will they deduct a cancellation fee?

Important Clauses in a Sale Deed

The Sale Deed is your permanent record. Ensure these details are correct:

- Buyer and Seller Details: Your name, your father’s name, and your address must be spelled exactly as they appear on other official documents like your PAN card and Aadhaar.

- Property Description: This should be precise. It must include the survey number, plot number, floor number, built-up area, and common areas. For an apartment, it should mention the exact dimensions.

- Sale Consideration: This states the final amount you paid. It is important for future reference, especially if you ever want to sell the property and need to calculate your capital gains.

- Indemnity Clause: This is your safety net. It is the seller’s promise to compensate you if you suffer a loss because their title to the property was defective. For example, if a long-lost relative of the seller shows up and claims they own half the property, the seller is legally bound to defend you and cover your costs.

- Possession Confirmation: This clause formally records that the seller has handed over the vacant and physical possession of the property to you.

Registration Process for a Sale Deed

Registering the Sale Deed is a must. Here is how it works in simple steps:

- Draft the Sale Deed: You or your lawyer will prepare the final Sale Deed document based on the terms of the Agreement to Sale.

- Pay the Stamp Duty: You need to buy non-judicial stamp paper of the correct value. In many states, you now pay the stamp duty online through designated banks or portals. The amount is a percentage of the property’s value.

- Visit the Sub-Registrar Office: Both the buyer and seller need to go to the Sub-Registrar’s office where the property is located. You have to be there in person. Take two witnesses with you. They must have their own ID proofs.

- Sign and Submit: The buyer, seller, and both witnesses sign the Sale Deed in front of the Sub-Registrar. Your photographs and fingerprints are also taken. The document is then submitted along with the required fees.

- Get it Registered: The Sub-Registrar enters the details into the official register. The original registered Sale Deed is usually returned to you within a few weeks. This is your legal proof of ownership.

Risks of Not Understanding the Difference

I have seen people make this mistake, and it never ends well. Not knowing the difference can lead to:

- Ownership Disputes: The biggest risk. You might pay almost all the money, live in the house for years, but if only an agreement to sale was signed and not a registered sale deed, you are not the legal owner. The seller could technically still sell it to someone else.

- Financial Loss: If the deal falls through for any reason, and your rights aren’t clearly documented in the agreement to sale, you could lose your deposit and all the installments you paid.

- Project Delays: The agreement to sale is your only tool to hold a builder accountable for delays. If your agreement is poorly written, the builder can delay possession for years without any penalty.

- Legal Complications: If the seller dies before executing the sale deed, their legal heirs might not feel bound by the agreement. You could end up in a long, expensive court battle with them.

Common Mistakes Buyers Make

Let’s look at some simple mistakes that can cause big problems.

- Assuming Agreement = Ownership: This is number one. People sign the agreement, pay the money, and think “I own this place.” They don’t. They have only bought a promise.

- Not Registering Documents: Some buyers don’t register the agreement to sale to save a few thousand rupees in stamp duty. This is false economy. If the seller cheats you, an unregistered agreement is much harder to enforce in court.

- Ignoring Legal Clauses: Legal documents can be boring and hard to read. But skipping through them is dangerous. A vague clause about “super area” in an agreement to sale could mean you end up paying for spaces you can’t even use.

- Not Verifying Property Title: You rely on what the seller or builder tells you. You don’t hire a lawyer to independently check if the seller actually owns the land and has the right to sell it. This is a critical step before you sign anything.

Tips for Buyers and Property Owners

Here is some practical advice to protect yourself.

- Always Verify Title Documents: Before you pay a single rupee, hire a good property lawyer. Ask them to check the seller’s title documents. They will trace the ownership history for the last 30 years to ensure it’s clean.

- Register the Sale Deed Properly: Don’t try to save money by underpaying stamp duty or skipping registration. It is a legal requirement. A registered sale deed is your strongest shield.

- Consult a Legal Expert: Real estate law is complex. A good lawyer is worth their fee. They will explain the clauses in both the agreement to sale and the sale deed. They will tell you what is fair and what is not.

- Ensure All Payments Are Documented: Never pay in cash. Always pay by cheque or bank transfer. This creates a clear paper trail. For every payment you make, get a signed receipt from the seller or builder.

Conclusion

So, there you have it. The difference is clear.

An Agreement to Sale is a promise. It is the plan. It sets the terms for a future deal.

A Sale Deed is the proof of ownership. It is the final action. It makes you the legal owner.

Understanding this simple difference is the key to a safe and successful property purchase. It helps you avoid legal risks and financial disputes. It gives you the confidence to know exactly where you stand at every step of the journey.

Buying a home should be a happy experience. Knowing your documents ensures it stays that way.

FAQs

What is the main difference between agreement to sale and sale deed?

An agreement to sale is a promise to transfer property in the future. It creates an obligation on the seller. A sale deed is the actual transfer of ownership. It completes the transaction. One is a commitment. The other is the final action.

Does an agreement to sale mean I own the property?

No, it does not. You only have a right to demand ownership later. The seller remains the legal owner until the sale deed is executed and registered. Think of it like booking a hotel room. You have a reservation, but you don’t own the room yet.

Is it mandatory to register an agreement to sale?

Registration is not always mandatory, but it is strongly recommended. It depends on your state laws. However, if the agreement gives you possession of the property, registration becomes compulsory. A registered agreement offers better legal protection if disputes arise later.

Can I sell a property with only an agreement to sale?

No, you cannot. The agreement to sale does not make you the owner. You need a registered sale deed in your name to prove ownership. Only then can you legally sell the property to someone else. The sale deed is your title document.

What happens if the seller backs out after agreement to sale?

You can take legal action. The agreement to sale is a binding contract. You can approach court and ask for specific performance. This means the court can force the seller to complete the sale. Alternatively, you can claim damages for the breach of contract.

How much stamp duty is paid on each document?

Stamp duty on an agreement to sale is generally low. It is often a fixed nominal amount. Stamp duty on a sale deed is high. It is a percentage of the property’s value, usually between five to seven percent depending on your state. This is a major cost.

Is a sale deed valid without registration?

No, it has very little legal value. Under the Registration Act, a sale deed must be registered to be valid. Without registration, ownership does not legally transfer to you. The document exists, but it cannot be used as primary proof of title in court.

When should I sign the agreement to sale?

Sign it at the very beginning of the transaction. Sign it after you have verified the seller’s title documents but before you make any major payment. It secures the deal and sets clear terms for payment schedules, possession date, and what happens if things go wrong.

Can an agreement to sale be cancelled?

Yes, it can be cancelled. The cancellation terms are usually written in the agreement itself. It might happen if you fail to pay on time or if the seller cannot deliver possession. The document should clearly state the refund and penalty conditions for cancellation.

Which document is more important for a home loan?

Banks need both, but the sale deed is crucial for loan disbursement. The agreement to sale is needed to process the loan application and understand the terms. However, the bank disburses the final payment only after the sale deed is ready for registration.

0 Comments