If you are an NRI, here is what you need to know upfront.

You are required to file an Income Tax Return in India if your total taxable income from Indian sources exceeds ₹2.5 lakh in a financial year. Even if it does not cross that limit, you may still want to file, especially if TDS has been deducted on your NRO interest, rent, or capital gains and you want that money back.

NRI taxation in India is governed by the Income Tax Act, 1961. The rules are clear. As an NRI, you pay tax only on income earned or received in India. Your foreign salary, your overseas investments, none of that is India’s business. But rental income from your flat in Delhi, interest on your NRO account, dividends from Indian stocks, capital gains from selling property or mutual funds, all of that is taxable here.

The form you use matters too. Most NRIs file ITR-2. If you have business or professional income in India, you move to ITR-3. ITR-1 is not an option for NRIs at all.

This guide covers everything you need for AY 2026-27. Which ITR form to pick. What income to declare. The tax rates on capital gains. Key exemptions including Section 115F. The 90% rule. DTAA benefits. And the step-by-step filing process with deadlines. MostlyNRI’s advisory team put this together so you have one clear resource, not ten confusing ones.

Do NRIs Need to File an Income Tax Return in India?

Yes, if your taxable income from India exceeds ₹2.5 lakh in a financial year, you must file an ITR. This is true even if you have been living abroad for years. The key is where the income comes from, not where you live.

Here is what counts as India-sourced income for an NRI:

- Rental income from property in India

- Capital gains from selling Indian assets (property, stocks, mutual funds)

- Interest earned on NRO accounts

- Dividends from Indian companies

- Any salary income for services rendered in India

Income you earn abroad, your foreign salary, your overseas investments, none of that is taxable in India as an NRI. India only taxes what is earned or received here.

Think of it like this. You have two buckets. The Indian bucket and the foreign bucket.

If your Indian bucket has more than ₹2.5 lakh in a year, you file. If it does not, you may still want to file to claim a refund on TDS that was deducted from your NRO interest or rental income.

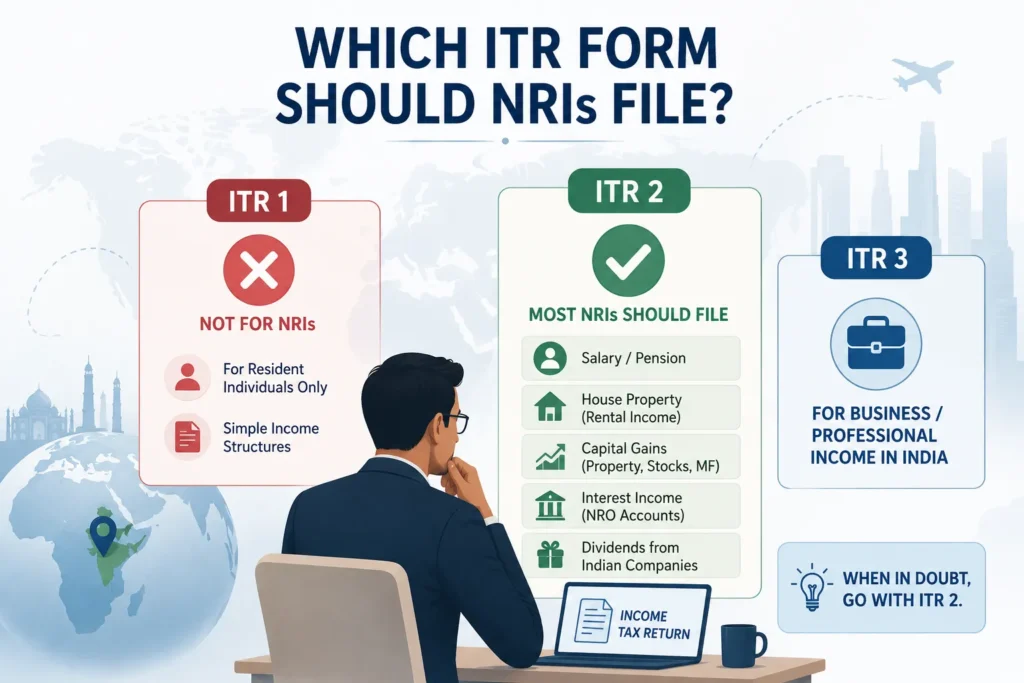

Which ITR Form Should NRIs File: ITR 1 or ITR 2?

This is one of the most commonly confused points. Let us make it very simple.

NRIs cannot file ITR 1: ITR 1, also called Sahaj, is only for resident individuals with simple income structures. NRIs are categorically excluded from using it, even if their income in India is straightforward.

ITR 2 is the correct form for most NRIs. It covers:

- Income from salary or pension

- Income from house property (rental income)

- Capital gains from property, stocks, or mutual funds

- Interest income from NRO accounts

- Dividends from Indian companies

If you run a business or have professional income in India, you would use ITR 3 instead.

For the vast majority of NRIs filing for AY 2026-27, ITR 2 is your form. When in doubt, go with ITR 2.

What Income Is Taxable for NRIs in India?

Let us go through each major income type. Each one has different tax treatment, so it helps to understand them separately.

Rental Income from Indian Property

If you own a flat, a shop, or any property in India and it earns rent, that income is taxable. Even if you have been living in Canada for ten years.

Here is the good news. A standard deduction of 30% is automatically applied to your rental income. This is meant to cover maintenance and repair costs. You do not have to prove expenses.

Your tenant is supposed to deduct TDS before paying you. If they have done that correctly, tax has already been paid on your behalf. But you still need to declare this income in your ITR. And if the TDS deducted is higher than your actual tax liability, you may be eligible for a refund.

Capital Gains: Property, Mutual Funds, and Stocks

This section matters a lot for NRIs who sell assets in India.

Short-term capital gains (STCG) apply when you sell assets before the holding period threshold. For equity (stocks and equity mutual funds), that threshold is 12 months. For property, it is 24 months.

Long-term capital gains (LTCG) apply after those periods.

Applicable tax rates depend on the prevailing Finance Act and the date of transfer. For AY 2026-27, the applicable rates are:

| Asset Type | STCG Rate | LTCG Rate |

|---|---|---|

| Listed equity / equity mutual funds | 20% | 12.5% (above ₹1.25 lakh) |

| Property | Slab rate | 12.5% (without indexation) |

| Debt mutual funds | Slab rate | Slab rate |

Note: Tax rates are subject to change per the Finance Act. Always verify on the Income Tax India portal or consult a tax advisor.

For NRIs, TDS is usually deducted at source on capital gains from property transactions. The buyer is responsible for deducting and depositing this TDS. You declare the gains in your ITR and claim credit for TDS already paid.

Dividends from Indian Companies

Dividends from Indian companies are taxable in your hands as an NRI. The company deducts TDS before paying out the dividend.

Here is where it gets useful. If India has a Double Taxation Avoidance Agreement (DTAA) with your country of residence, you may be able to reduce the tax rate on dividends. For example, India’s DTAA with the UAE or the UK may allow a lower tax rate than the standard domestic rate.

To claim DTAA benefits, you need to submit a Tax Residency Certificate (TRC) from your country of residence and fill in the relevant schedule in ITR 2.

Interest on NRO Accounts

NRO account interest is fully taxable in India. TDS is deducted at 30% (plus surcharge and cess) before the interest is credited to your account.

Many NRIs assume that because TDS was already deducted, they do not need to declare it. That is not correct. You must still include this income in your ITR. The TDS deducted will be credited against your total tax liability, and if it exceeds what you actually owe, you get a refund.

Contrast this with NRE accounts. Interest on NRE accounts is completely tax-exempt in India. Not subject to TDS. Not required to be declared. This is a significant difference between the two account types.

Key Exemptions and Deductions Available to NRIs

NRIs do not get all the deductions that resident Indians get. But there are still meaningful benefits available.

Section 80C deductions are available to NRIs, but with limitations. You can claim deductions for life insurance premiums, repayment of home loan principal, and investments in ELSS mutual funds. However, Public Provident Fund (PPF) accounts cannot be opened by NRIs, and certain other 80C instruments are not available.

DTAA benefits are significant. If you are a tax resident of a country that has a DTAA with India, you can claim relief to avoid being taxed on the same income twice. The DTAA specifies which country has the right to tax specific income types, or caps the rate at which each country can tax.

Section 115F: Capital Gains Exemption for NRIs

This one deserves special attention. Section 115F is one of the most underused exemptions available to NRIs, and most generic blogs skip over it entirely.

Here is what it does. If you sell a foreign exchange asset, and reinvest the sale proceeds into specified assets within six months, you can claim exemption on the long-term capital gains. You do not pay capital gains tax on that sale.

Foreign exchange assets in this context include shares in Indian companies, debentures of Indian companies, and deposits in Indian banks, when these were purchased using foreign currency.

The proceeds need to be reinvested into specified assets such as shares or debentures of Indian companies, or into savings certificates as defined under the Public Provident Fund Act.

There is a condition. If you sell the new asset within three years of buying it, the capital gains exemption is reversed and becomes taxable in that year.

Think of it as the government saying: We will not tax you on that gain, as long as you keep the money invested in India.

If you are an NRI who has sold shares or debentures that were bought with foreign currency, talk to a tax advisor about whether Section 115F applies to your situation before filing.

What Is Jurisdiction of Residence for NRIs and Why Does It Matter?

When you file ITR 2 as an NRI, the portal asks you to declare your jurisdiction of residence. This simply means: which country do you officially live in for tax purposes?

This is not just a formality. It determines which DTAA applies to your income, and how much credit or exemption you can claim.

For example, if you are a tax resident of the UAE, and India has a DTAA with the UAE, you can claim that treaty’s benefits when filing your Indian ITR. The treaty may reduce the TDS rate on your NRO interest or dividends.

To declare your jurisdiction of residence correctly, you need:

- Your country of residence as per your visa or resident status

- A Tax Residency Certificate (TRC) issued by the tax authority of your country of residence

- Form 10F, a self-declaration form that must be filed on the Income Tax portal if certain details are missing from your TRC

Getting this wrong can mean you miss out on DTAA benefits, or worse, face scrutiny from the tax department. Fill it in carefully.

Step-by-Step: How to File ITR as an NRI for AY 2026-27

Here is the actual process, simplified.

Step 1: Register or log in to the Income Tax e-filing portal

Go to Income Tax Official website. Use your PAN to register or log in. Your PAN is your primary identifier throughout this process.

Step 2: Gather your documents

You will need: Form 16A or TDS certificates, bank statements for all NRO and Indian accounts, details of capital gains (contract notes or sale deeds), dividend statements, rental income records, TRC and Form 10F if claiming DTAA benefits.

Step 3: Select ITR 2

Under the filing section, choose Assessment Year 2026-27 and select ITR 2 as your form. Do not use ITR 1.

Step 4: Fill in your residential status

Select Non-Resident under residential status. This changes which schedules appear in the form. Fill in your jurisdiction of residence and passport details.

Step 5: Enter income details by category

Declare rental income under house property. Enter capital gains in the CG schedule. Add NRO interest under other sources. Declare dividend income separately.

Step 6: Claim deductions and DTAA benefits

Enter Section 80C deductions if applicable. Claim DTAA relief under the relevant schedule. Mention TDS credits from Form 26AS or AIS.

Step 7: Verify and submit

After filling in all details and computing your tax, submit the return. Then e-verify it.

E-verification options for NRIs:

- Net banking (if you have an Indian bank account with net banking enabled)

- Aadhaar OTP (only if your Aadhaar is linked to an active Indian mobile number)

- Sending a signed physical ITR-V to CPC Bengaluru within 30 days of filing (this is the most reliable option for NRIs without an active Indian number)

The filing window for AY 2026-27 opened on April 1, 2026. The standard deadline for most NRIs is July 31, 2026. This deadline is subject to extension by the Income Tax Department, so always check the official portal for updates.

Frequently Asked Questions

Can I file ITR for AY 2026-27 now?

Yes. The filing window for AY 2026-27 opened on April 1, 2026. The standard deadline for NRIs not requiring audit is July 31, 2026. Check the Income Tax India portal for the latest dates as extensions are common.

Do NRIs need to file an income tax return in India?

Yes, if your India-sourced taxable income exceeds ₹2.5 lakh per year. This includes rent, capital gains, NRO account interest, and dividends from Indian companies.

What is the 90% rule for non-residents?

If 90% or more of your total global income comes from India, you are treated as a resident individual for tax purposes. This can affect your tax slab benefits and eligibility for certain exemptions.

How much income is tax-free for NRIs in India?

NRIs have a basic exemption of ₹2.5 lakh under the old tax regime. Unlike resident senior citizens, NRIs do not get higher age-based exemptions. NRE account interest and FCNR deposit interest are fully tax-exempt.

When can we file ITR for assessment year 2026-27?

Filing opened on April 1, 2026. The due date is typically July 31, 2026, for NRIs not requiring an audit. Always verify on the Income Tax India portal.

Do I need to file ITR 1 or ITR 2 for NRIs?

NRIs must file ITR 2. ITR 1 is not available to NRIs. ITR 3 applies if you have business or professional income in India.

What is the new rule for NRI in India for AY 2026-27?

Key changes include updated LTCG and STCG rates on equity and mutual funds, revised property TDS rules, and changes to DTAA claim procedures on the e-filing portal. Review the Finance Act or speak with a tax advisor for your specific situation.

Conclusion

NRI tax filing does not have to be complicated. Once you know the basics, the path is clear.

File ITR 2. Declare all India-sourced income whether rental, capital gains, NRO interest, or dividends. Claim Section 115F exemption if it applies to your situation. Use DTAA benefits to avoid double taxation. And submit before July 31, 2026.

If you want to skip the back-and-forth with the portal and make sure you are not missing any deduction, MostlyNRI’s tax advisory team handles NRI ITR filing end-to-end. From form selection to e-verification.

Disclaimer: Tax laws change frequently and vary based on individual circumstances. Consult a qualified tax advisor before filing.

0 Comments