Owning a house in one’s home country is not just a great investment. For Non-Resident Indians (NRIs) especially, it translates into a powerful emotional connect with one’s roots. In practical terms too, investing in real estate remains one of the most valued assets for Indians at home and overseas.

Check this: The Indian Real Estate Industry Report estimates that the real estate market is likely to grow to a mammoth US$ 9.30 billion by 2040 from just US$ 1.72 billion in 2019. By 2025, the sector is projected to contribute 13% to India’s GDP.

Real estate investment helps build wealth consistently, particularly through rental income. However, it’s not an easy path to navigate. From ensuring the right tenant and payment of rents on time, to various laws to do with renting out property in India, there’s a labyrinth of issues that need to be understood to allow for a hassle-free experience.

A basic knowledge of India’s extensive taxation rules and regulations is mandatory. A key aspect is the policy of Tax Deducted at Source or TDS on income – in this case, TDS on rent payment for properties.

Here’s a quick guide and 101 for deciphering the fundamentals of TDS on rental properties in India that will serve as a reliable handbook for Indian as well as NRI owners/landlords.

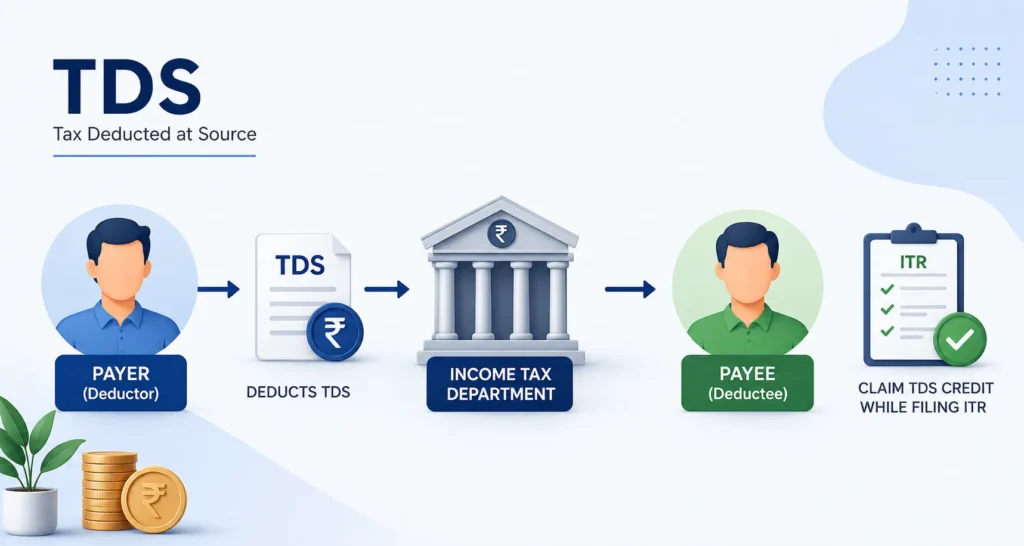

What Is TDS Or Tax Deducted At Source?

TDS, a part of income tax is a mechanism introduced to directly collect taxes from the source of income or at the time when the income is paid out. According to India’s tax system, TDS is a vital factor in taxation because it has a substantial influence on taxpayers. It is a process of collecting income tax by the government and offers ease to the deductee (receiving the payment) as it gets subtracted automatically, thus also significantly lowering tax evasion.

Before making a payment to an individual, the deductor (paying the rent) deducts and pays tax on the individual’s behalf to the Income Tax department. An individual can claim or adjust TDS credit while filing their income tax return against income tax payable

Understanding What Rent Implies

Rent under any formal agreement, including a registered rent agreement, is any payment that is made for using/occupying the following:

- Buildings, inclusive of factory buildings

- Land

- Land pertinent to any building inclusive of factory buildings

- A plant such as an industrial or manufacturing facility

- Equipment such as tools, computer systems, networks, other infrastructure required for running a business

- Machinery

- Fittings and furniture

In India, TDS on rent payment falls under Section 194-I of the Income Tax Act. Tax deducted at source or TDS is required to be deducted by the person paying the rent from the rent payable and paying it to the government.

TDS Provisions For NRI Owner/Landlord

A person who is of Indian origin or is a citizen of India but does not reside in India is known as an NRI. The residential status of said individual will be determined under Section 6 according to which, said person is a resident of India if he satisfies any of the following conditions:

- Has resided in India for a minimum period of 182 days during the previous year.

- Has resided in India for a minimum period of 60 days during the previous year and a minimum of 365 days during 4 previous years.

- In this regard, an NRI is a person who does not satisfy any of the above criteria.

Tenants paying rent on properties that are owned by NRIs are required to deduct 31.2% tax at source and submit the aggregate amount to the tax authorities. In the case of rent payments to NRIs, the tenant must fill in Form 15CA and submit it online to the income tax department. In such cases, TDS is mandatory on the rent that is paid irrespective of the amount payable.

- Tenants must get a Tax Account Number or TAN via the NSDL website (https://tin.tin.nsdl.com/tan/form49B.html)

- Once the TAN is received, the tenant can deduct tax every month and pay the remaining amount to their landlord.

- The tax deducted at source from rent paid in a particular calendar month must be submitted by the 7th of the following month.

- Please note, TDS must be paid on time, else it invites action under Section 276B of the Income Tax Act, 1961. It may even lead to imprisonment ranging from 3 months up to 7 years.

- If an individual fails to deduct tax from the rent paid to an NRI landlord, they might attract a penalty equal to the tax not deducted as per Section 271C of the Income Tax Act.

- It is obligatory for tenants to fill Form 15CA on the income tax portal every time rent is paid.

- If the total rent paid per annum exceeds Rs.5 lakh, the tenant must obtain Form 15CB from a Chartered Accountant.

When one rents a place, it is their responsibility to find out if the landlord is an NRI. This makes it easy for them to deduct TDS on the rent paid and adhere to the Income Tax Act.

Here’s a quick example to illustrate:

Mr. R is an NRI and owns a residential property in Bangalore. He has lent this property to Mr. and Mrs. D who pay a monthly rent of Rs 8,000. Mr. D knows that Mr. R is an NRI, and he deducts 31.2% from the monthly rent and deposits it into his TAN. Therefore when Mr. D paid the rent for June on 1st July, he deducted Rs 2,496 from the rent and deposited the amount within 7th August to his tax account online. The remaining sum of Rs 5,504 is transferred to the NRI landlord’s account.

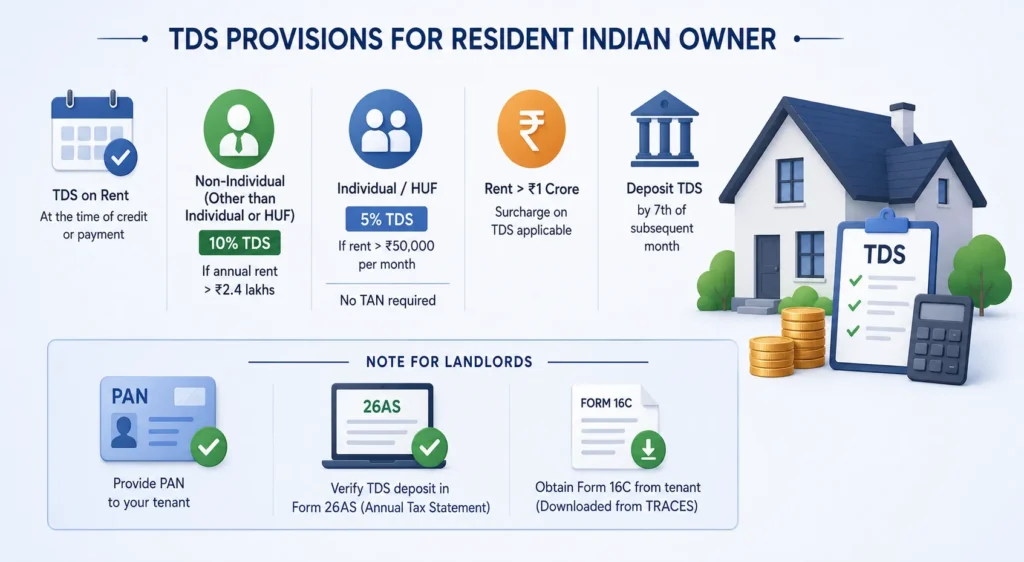

TDS Provisions For Resident Indian Owner

Tax is required to be deducted at source at the time of credit of ‘income by way of rent’ to the account of the receiver or when the payment is being made.

As per section 194-I of the Finance Act, 2017, a person (not being an individual or HUF*) who is responsible for paying rent is liable to deduct 10% of the annual rent as TDS if the annual rent exceeds Rs 2.4 lakhs.

*An HUF or a Hindu Undivided Family is treated as a ‘person’ under Section 2(31) of the Income Tax Act of 1961 and is a family that consists of all persons lineally descended from a common ancestor and includes their wives and unmarried daughters. There is no contract to create a HUF, it is created automatically in a Hindu Family. Jain and Sikh families, although, are not governed by the Hindu Law are treated as HUF under the Act.

- In the event one belongs to the Individual or HUF category, they can deduct TDS at 5% if the rent that they are giving exceeds Rs. 50,000 per month.

- Also, such Individuals and HUF liable to deduct TDS at 5% need not apply for TAN.

- If the total amount is more than Rs. 1 crore, a surcharge to the TDS also needs to be added.

- The Tax Deducted at Source must be deposited to the government by 7th of the subsequent month.

If you are a landlord of a property, please make a note of these points:

- Provide your PAN to the tenant for furnishing information with regards to TDS to the Income Tax Department.

- Verify deposit of taxes deducted by the tenant in your Form 26AS in your Annual Tax Statement.

- Insist on obtaining Form 16C from the tenant which has been downloaded from the TRACES website only which is the TDS Reconciliation Analysis and Correcting Enabling System in India.

Final Thoughts…

Even though TDS is just a small aspect of India’s massive taxation system, it is imperative we understand its nuances and benefits. This guide should help you navigate India’s rental system and the TDS taxation attached to it.

Also Read: Rules Pertaining to TDS Deduction by Tenants for NRI-Owned Properties

0 Comments