Selling property in India can be a profitable venture, but it’s essential to understand the tax implications associated with it. One of the most significant considerations is capital gain tax, which is levied on the profit you make from the sale of a capital asset, such as property. In this blog, we’ll break down the capital gains rules for property sales in India, including what capital gains are, the types of capital gains, applicable tax rates, exemptions, and tips for tax planning. Lets understand the capital gains tax calculator on sale of property.

What are Capital Gains?

Capital gains are the profits earned when you sell a capital asset, like real estate, at a price higher than the purchase price. These gains are classified into two types based on the duration you hold the asset before selling:

- Short-Term Capital Gains (STCG): If the property is held for less than 24 months (2 years) before selling, it falls under short-term capital gains.

- Long-Term Capital Gains (LTCG): If the property is held for more than 24 months, it qualifies as long-term capital gains.

This classification is essential as it impacts the tax rate and available exemptions.

Capital gains tax calculator on sale of property

The tax rates for capital gains on property sales differ for short-term and long-term holdings:

- Short-Term Capital Gains Tax: STCG on property is taxed at the individual’s applicable income tax slab rate. This means that short-term gains are added to your income for the year and taxed as per your slab rate.

- Long-Term Capital Gains Tax: LTCG on property sales is taxed at a flat rate of 20% after indexation. Indexation is the process of adjusting the purchase cost based on inflation, which reduces the taxable gains and, subsequently, the tax payable.

Calculating Capital Gains:

Calculating capital gains involves determining the sale price, purchase price, and any improvement costs. Here’s a step-by-step outline of the calculation process for short-term and long-term gains:

For Short-Term Capital Gains:

1. Calculate the Sale Price: Sale Price = Total amount received from the sale of the property.

2. Deduct the Purchase Cost and Expenses: This includes the original purchase price, brokerage, stamp duty, legal fees, and any improvement costs.

Formula: Short-Term Capital Gains = Sale Price – (Purchase Price + Expenses)

For Long-Term Capital Gains:

1. Calculate Indexed Cost of Acquisition: Purchase Price × (Cost Inflation Index of the year of sale ÷ Cost Inflation Index of the year of purchase).

2. Subtract the Indexed Cost from Sale Price.

Formula: Long-Term Capital Gains = Sale Price – (Indexed Purchase Cost + Expenses)

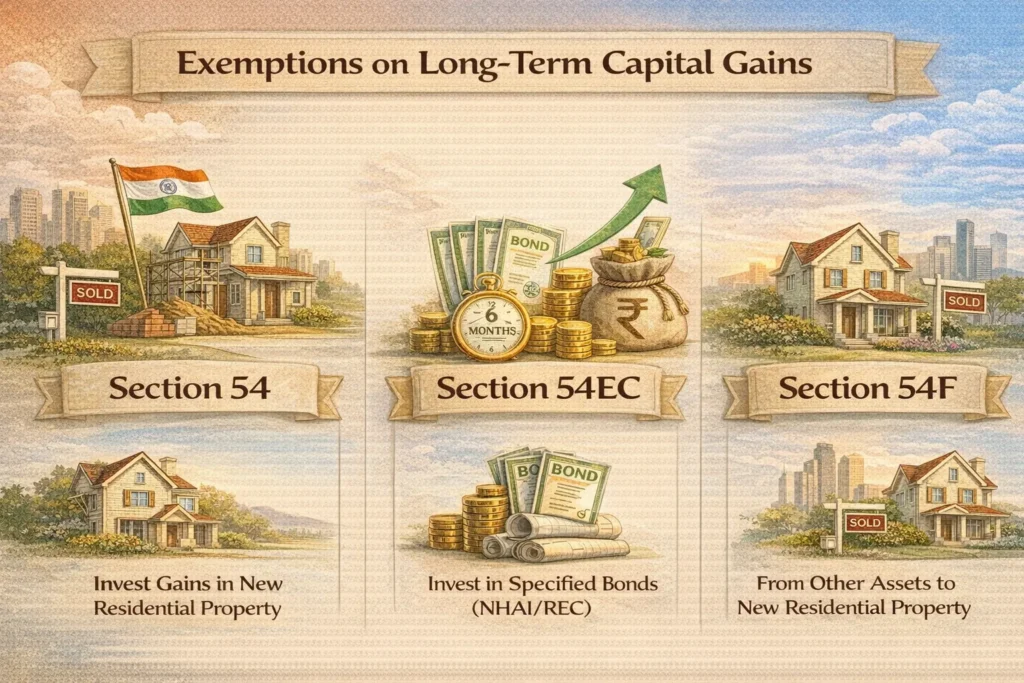

Exemptions on Long-Term Capital Gains:

To encourage investment and reinvestment in real estate and specific financial products, the Indian tax system provides several exemptions under Sections 54, 54EC, and 54F for long-term capital gains.

- Section 54: If you sell a residential property and invest the capital gains in purchasing or constructing another residential property, you can claim an exemption. The new property must be bought within 1 year before or 2 years after the sale, or constructed within 3 years.

- Section 54EC: This allows you to invest up to Rs. 50 lakhs of your long-term capital gains in specific bonds (such as those from NHAI or REC) within six months of the sale. These bonds have a lock-in period of 5 years.

- Section 54F: If you sell any long-term capital asset other than a residential property and use the proceeds to buy a new residential property, you can claim an exemption. However, certain conditions apply, such as not owning more than one residential property at the time of investment.

Special Considerations and Tips:

- Joint Ownership: If the property is jointly owned, the capital gains can be split based on the ownership ratio, potentially reducing the tax burden.

- Set-off and Carry Forward of Losses: Capital losses, if any, from property sales can be set off against capital gains. Unutilized losses can be carried forward for up to eight assessment years.

- Tax Planning for NRIs: Non-resident Indians (NRIs) are also subject to capital gains tax on property sales, but the rules may vary slightly, especially in terms of TDS (Tax Deducted at Source).

Filing Capital Gains Tax:

Capital gains from property sales should be disclosed in your income tax return (ITR) under “Capital Gains.” To avoid complications, make sure you keep records of all documentation, including purchase agreements, sale deeds, and improvement costs.

Conclusion:

Navigating capital gains tax on property sales in India can seem complex, but understanding the basics can help you make informed financial decisions. By planning your sale strategically, taking advantage of available exemptions, and consulting with tax professionals when needed, you can reduce your tax burden and maximize your gains. Whether you’re selling property to upgrade, downsize, or for investment purposes, knowing the capital gains tax rules will ensure a smoother, tax-efficient transaction.

Also Read: Documents Required To Sale Property In India

0 Comments